- Edited

Summary

We are in a period of strong demand for OHM, as evidenced both by price appreciation and the treasury’s rapid accumulation of reserve and liquidity assets. Given current market conditions, and looking to the future of OHM as a trading pair, the Policy team believes that it’s the perfect time to launch an OHM-ETH liquidity pool and bond, which will allow us to capture additional volume and fees.

Motivation

We believe an OHM-ETH pool is a natural next step for Olympus. One of the Policy team’s ongoing goals is to maintain a healthy amount of liquidity relative to our growing market cap. A relatively large OHM-ETH pool would help accomplish this, while also routing more trading flow through our pools, allowing our treasury to capture more fees in this period of strong market demand. Since ETH is currently one of the most common counter-pairs in DeFi, directly pairing OHM to it also opens up routing rails of pairs not directly tied to the OHM token.

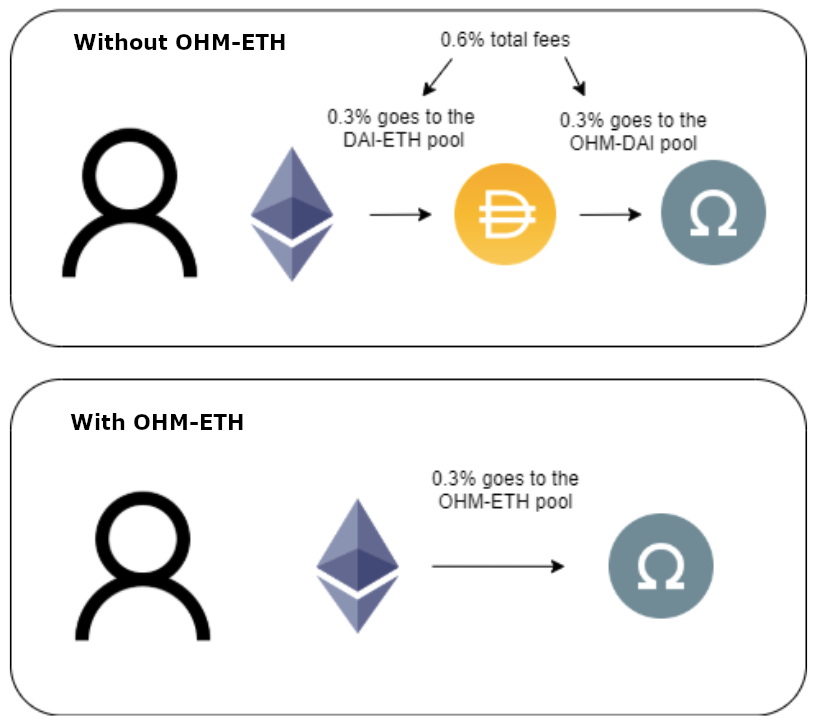

For example, a user currently swapping from ETH to OHM would route from ETH -> DAI -> OHM. Not only does this cause the user to experience double the trading fees (0.6% vs 0.3%), Olympus would only capture half of these fees as well. The creation of an OHM-ETH pool would reduce the fees for the user, and allow us to capture all fees from this route.

On the 15th of October, trades through the OHM-DAI pool generated $175m in additional volume for other Sushiswap pools, $136m of that for the DAI-ETH pool.

The Olympus community has shown strong support and enthusiasm for accumulating more ETH in the treasury. We believe that increased ETH price exposure from creating the proposed liquidity pool is justified by the benefits of having this pool. It’s time we put our ETH to productive work!

Proposal

Match $2.5M worth of DAO OHM with $2.5M worth of Treasury ETH ($5m total liquidity) for the initial LP position to bootstrap the pool. At current prices we have $6,807,721 ETH in the Treasury. This wouldn't affect treasury RFV in any way. The alternative to this would be paying out OHM incentives to liquidity providers to launch the pool, which would just increase the cost to the protocol.

Launch an OHM-ETH bond

Target an initial $100m in liquidity accumulated over a minimum of 4 weeks. Depending on market conditions the Policy team would speed up or slow down this process, but the target would not be reached before 4 weeks.

After that, maintain 20% of our total liquidity in the OHM-ETH pool

The ETH portion of this pool would be in addition to the targets for ETH as a reserve asset in treasury, which has a separate allocation target, outlined by OIP-15 (and its amendments)

Note: ETH mentioned in this proposal is actually wETH (wrapped ETH).

Vote

For (1): Bootstrap OHM-ETH pool as proposed and launch OHM-ETH bond

For (2): Don't bootstrap OHM-ETH pool, but launch OHM-ETH bond. In this case we'd have to pay OHM incentives to LPs to launch the pool.

Against: Do nothing